Is Thailand the next Johor?

Thailand is matching Johor's explosive data centre growth trajectory.

Thailand is entering a breakout phase, according to DC Byte's latest market report. Is the Land of Smiles set to become the next Johor with off-the-charts growth?

I was in Thailand earlier this year to give a private presentation to a room of data centre practitioners. The landscape is a far cry from when I visited in 2014 on a data centre research trip. Back then, the market was dominated by local telcos and enterprise data centres. Today, Thailand attracting the world's biggest names in cloud and colocation.

At a tipping point

After seeing multiple waves of data centre optimism over the years, I've expressed scepticism about Thailand's potential as recently as last year. The market had promise but lacked the critical mass of hyperscale commitments that signal a true boom. However, things look quite different this round.

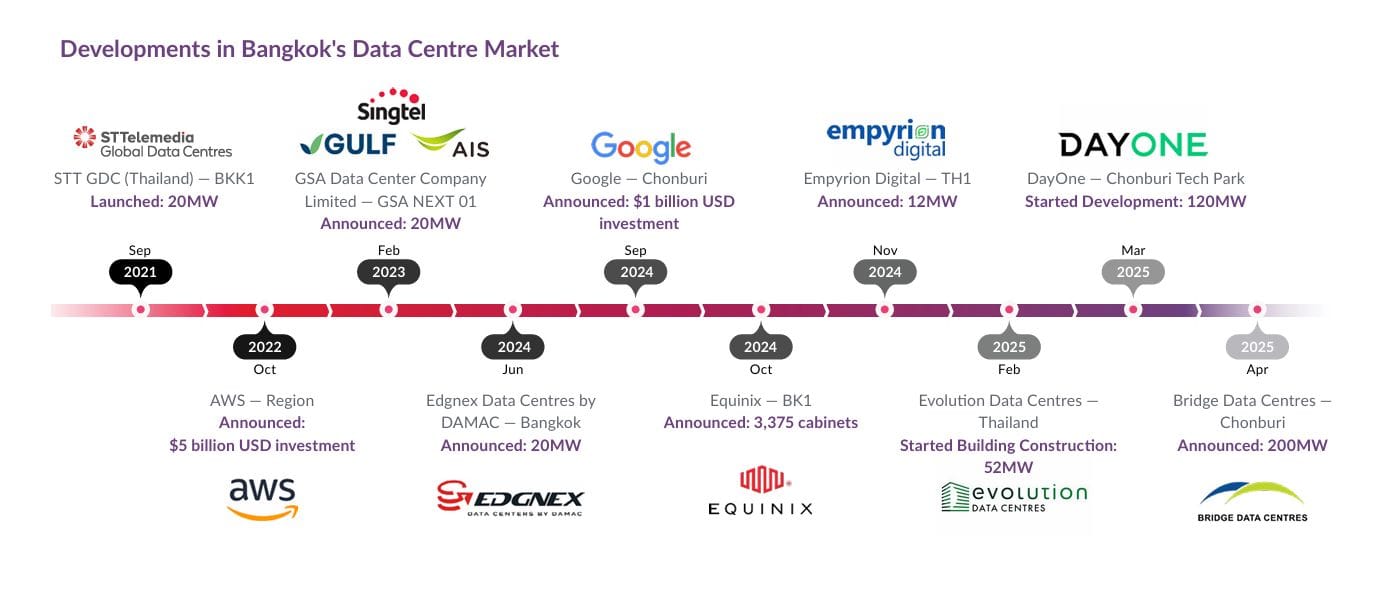

Multiple major players have announced their entry into Thailand over the last 12 months, with many well-established names building hyperscale facilities at unprecedented scale. Some of the largest developments, including projects by Google, DayOne, and Bridge Data Centres, are located in Chonburi, southwest of Bangkok. This clustering effect is reminiscent of how Johor's Sedenak Tech Park became a data centre hotspot.

Add in the various data centres that have broken ground since 2021, such as STT GDC, Equinix, and Empyrion Digital, and the capacity stacks up quickly. What's particularly telling is the mix of players: you have established Asian operators, global colocation giants, and hyperscale cloud providers all betting on the same market.

By the numbers

DC Byte's report lays out the hard numbers that matter: Bangkok's 2,587MW of IT capacity in the pipeline outpaces regional heavyweights, trailing only Malaysia in Southeast Asia.

To be absolutely clear, the 2,027MW here includes "early stage" builds, which might not actually be built. These are projects that have been announced but haven't broken ground yet. But you could have said the same about Johor a year ago, too. Many of those "speculative" projects are now under active construction.

The parallels are striking. Both markets went from relative obscurity to commanding international attention within a very short span of time. Both benefited from overflow demand from more established markets. And both offered compelling advantages: available land, government support, and crucially, access to power.

Cloud providers lead the charge

For now, the cloud is a strong driving force behind Thailand's data centre boom. Currently operational are AWS, Alibaba Cloud, Huawei Cloud, and Tencent Cloud. These providers have established a foundation that makes Thailand viable for enterprise workloads. Coming soon are GCP, Azure, and BytePlus, which will complete the roster of major cloud platforms.

This cloud provider diversity is crucial. It signals that Thailand isn't just a single-provider market but a strategic location that multiple platforms view as essential for their Southeast Asian operations.

DC Byte notes that the current live capacity stands at around 120MW, a modest base compared to the ambitious pipeline. Additional capacity is expected to come online by the end of the year as ongoing developments reach completion.

What do you think? Is Thailand the next Johor? The numbers suggest it's possible, but as always with data centre development, the proof will be in what actually gets built. DC Byte's free report can be accessed from Nicole Seah's blog post here.